Veteran-focused lender gains surpasses 1000 VA loan applications as new partnership gains national traction

Irvine, California – March 17, 2026 World Home Loans, a fast-growing, veteran-focused mortgage lender dedicated to delivering exceptional pricing and service for military homebuyers, today announced a strategic partnership with military.com, one of the largest digital platforms serving the U.S. military community. The partnership expands access to trusted VA home financing resources for service members, veterans and their families nationwide.

Through the partnership, VA borrowers engaging through Military.com will gain direct access to the World Home Loans lending platform, which provides highly competitive mortgage pricing, rapid response times and dedicated VA loan expertise designed specifically for military borrowers. On average, World Home Loans delivers rates approximately 0.50% lower than many traditional VA lenders, creating a meaningful pricing advantage for veterans pursuing homeownership.

“Veterans deserve better than what they often experience in this industry,” said Brian Cooke, CEO and Founder of World Home Loans. “Our partnership with Military.com allows us to reach veterans where they already turn for trusted information and connect them with lenders who truly understand the VA loan program.”

In the first two weeks of the partnership with Military.com, World Home Loans reports it has already received more than 1,000 VA loan applications, signaling strong early engagement from military households seeking clear guidance and competitive lending options. Military.com reaches millions of active-duty service members, veterans and military families each month, making it one of the most influential platforms serving the military community. Through the partnership with World Home Loans, the platform expands its ability to connect its audience with trusted lending resources while helping veterans better understand their VA home loan benefits and opportunities for homeownership.

“Our audience includes millions of service members, veterans and military families who rely on Military.com for trusted information,” said Rony Arzoumanian, President of Military.com. “Partnering with World Home Loans connects them with a lender focused on serving veterans.”

World Home Loans expects application volume to continue increasing as the partnership expands nationally in the coming months. The company is also continuing to expand its licensing footprint and operational capacity to meet growing demand while maintaining service standards aligned with its mission of serving the military community.

World Home Loans is a mission-driven mortgage company founded by Brian Cooke, one of the nation’s top VA loan originators. Built on efficiency, execution and client-first service, World Home Loans exists to deliver Victory on the Home Front for veterans and their families. With a vision to become America’s leading VA lender, World Home Loans blends performance-driven culture with a mission rooted in legacy. World Home Loans Inc. is an Equal Housing Lender. NMLS # 2726290. Additional information about World Home Loans is available at worldhomeloans.com

About Military.com

Military.com is one of the largest digital platforms serving the U.S. military community, reaching millions of active-duty service members, veterans, retirees and military families each month. The platform provides trusted news, benefits guidance, career resources and financial tools that help military households navigate service, transition and civilian life. For more information, go to military.com

Younger veterans are entering the housing market with different expectations, different financial pressures, and a far more strategic view of homeownership than previous generations.

Let’s talk about Veteran homeownership. The conversation is changing.

For decades, the point of VA loan programs has been largely viewed through a traditional lens. The idea was to help military families purchase stable homes for the long-term, and do it with favorable financing. That mission still matters, but today’s younger veterans are approaching housing with a very different mindset.

Cut to today: our young Vets are entering the market at a time of elevated rates, constrained inventory, higher consumer debt, and growing economic uncertainty. The landscape has changed, making this new group of potential borrowers think about homeownership more strategically than prior generations. What I increasingly see are younger veterans viewing real estate not simply as shelter, but as a long-term financial tool. That shift is reshaping both the opportunities and the responsibilities facing mortgage professionals.

A rethink: Financial pressure is changing borrower behavior

What’s going through Vets’ heads is not what was going through their head 10 years ago. The modern Veteran borrower faces a more difficult economic backdrop than many previous generations. Home prices relative to income remain elevated. Student debt and consumer debt levels are significantly higher. Affordability pressures have forced many buyers to rethink how and where they purchase homes. The kicker? At the same time, military families often maintain a higher degree of mobility than civilian households. Frequent relocations, changing career paths, and uncertainty around future assignments naturally influence how veterans think about housing decisions. As a result, flexibility has become increasingly important.

We need to change our approach to serve our Vets

Many younger veterans are no longer approaching homeownership as a permanent, once-in-a-lifetime decision. Instead, they are evaluating properties through a broader financial lens. They are asking how a purchase fits into future investment goals, rental income potential, and long-term wealth accumulation.

Some are using VA financing to purchase multi-unit properties. Others are thinking ahead about retaining homes as rental assets after future relocations. In many cases, they are leveraging the VA benefit multiple times throughout their lives rather than viewing it as a one-time opportunity.

That level of financial ambition is encouraging, but it also means borrowers need better education and more sophisticated guidance than ever before. And as a lender, that means you also have to be an educator as well.

Education remains the industry’s biggest challenge

One of the most persistent barriers facing veterans is still misinformation. I continue to speak with military borrowers who believe they need perfect credit or substantial savings to qualify for a home loan. Not true. Others are told by agents or lenders that VA financing weakens their offer in competitive markets. Not true. Those misconceptions continue to limit opportunity. We need to be the ones to bust those myths and open doors for our Veterans.

The reality is that VA loans remain one of the strongest financing products available. Zero-down financing, flexible underwriting standards, and competitive pricing give veterans meaningful advantages, particularly in a difficult affordability environment. All true.

Execution, however, matters. For them, a properly structured VA loan supported by full underwriting and strong communication can compete extremely effectively in today’s market. The problem is that not every lender or real estate professional understands how to position these loans correctly.

There is also a broader issue around financial literacy. Many service members transition out of the military without receiving meaningful education around credit management, debt, budgeting, or long-term homeownership planning. They may technically qualify for a mortgage yet still lack confidence in their ability to purchase a home. That uncertainty affects decision-making. You can bring clarity. The role of mortgage professionals today extends beyond simply qualifying borrowers. It increasingly requires helping veterans understand the big picture: how to use homeownership as part of a larger financial strategy. This is particularly important with younger borrowers who are highly informed digitally, but still need to know how to navigate complex financial realities for the first time.

The future of Veteran lending is specialization: Talking their talk and walking their walk

The next phase of Veteran homeownership will likely reward lenders who combine expertise, speed, and transparency.

Today’s borrowers expect efficiency. This digitally savvy group compares lenders aggressively, researches products online, and demands clear communication throughout the process. They are far less willing to tolerate delays or vague explanations than previous generations. That expectation is forcing the industry to evolve.

Technology will continue to improve the customer experience, but specialization will remain the true differentiator. Veterans benefit most when they work with professionals who deeply understand military housing needs, mobility considerations, and the full range of VA financing options.

There are still products within the VA ecosystem that many borrowers never hear about because their lender does not offer them. Adjustable-rate VA products, for example, can be highly effective for military families who expect future relocation orders or shorter ownership horizons.

The broader policy conversation around housing affordability will also remain important. Housing access is becoming one of the defining economic issues facing younger Americans, including Veterans. The challenge for policymakers and the industry alike will be expanding affordability without creating additional instability in the market.

For Veterans specifically, the solution starts with improving access to trustworthy information and transparent lending practices. That’s on you. Veterans have earned one of the most powerful homeownership benefits available anywhere in the market. The responsibility now falls on the industry to ensure borrowers fully understand how to use it.

The reality is, this younger generation of Veterans is already approaching homeownership differently. They are more strategic, more financially ambitious, and more focused on flexibility than prior generations. These are not military borrowers as they once were. The lenders who recognize that shift and adapt to it will help shape the future of military homeownership–and their business–for years to come.

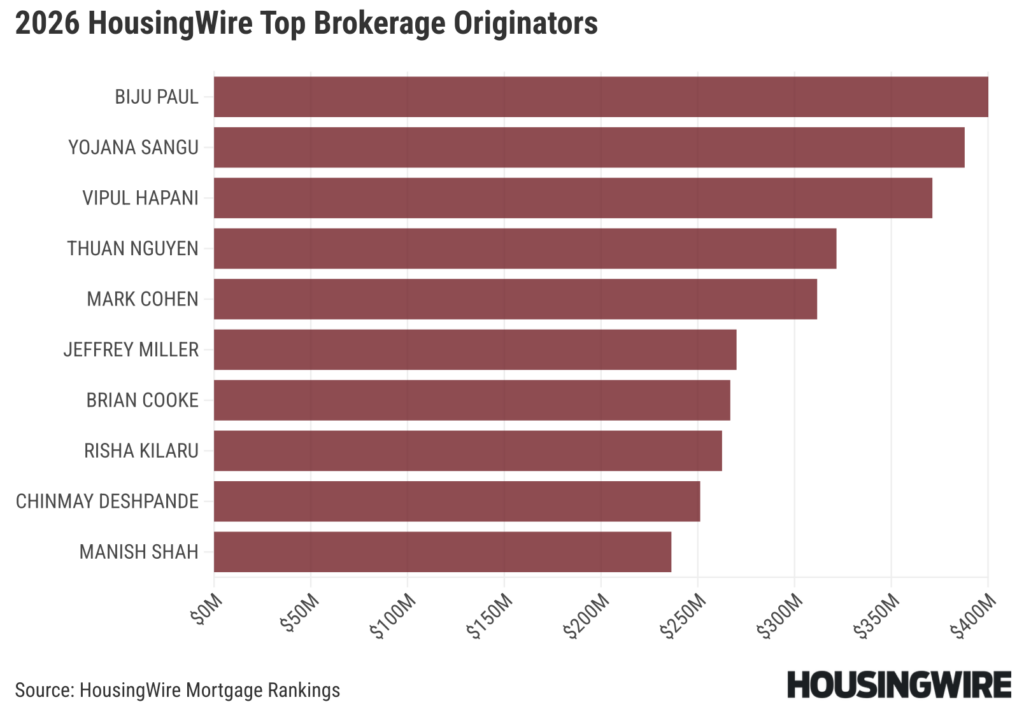

Brokers Brian Cooke, Vipul Hapani and Thuan Nguyen share their secret sauce in rising to the top of HousingWire’s inaugural rankings.

April 22, 2026, 12:54pm by Neil Piers on , Flávia Furlan Nunes and Sarah Wolak

Article Summary

HousingWire’s broker rankings place Brian Cooke No. 7 with $252.6 million across 668 loans in his first year running World Home Loans. HousingWire also profiles Vipul Hapani and Thuan Nguyen about scaling their purchase-driven production teams.

Brian Cooke wants his company to become the nation’s No. 1 mortgage brokerage for veterans and servicemembers who utilize U.S. Department of Veterans Affairs’ (VA) loan programs. Less than a year after launching World Home Loans, he’s well on his way to achieving that goal.

Cooke — who’s based in Southern California and licensed in 18 states — has been in the mortgage industry for more than 20 years, including stops at Provident Funding and Movement Mortgage. In 2018, he co-founded SunnyHill Financial, where he became one of the top brokers in the country across multiple loan products.

About three years ago, he began to chart a new course.

“It was Memorial Day 2023 when I had my all-in declaration that I would direct all my energy, efforts, marketing spend, to help make an impact for vets in America, because a lot of people out there complain that they get taken advantage of. But I wanted to actually do something about it,” Cooke said in an interview with HousingWire.

In his first year of business with World Home Loans, Cooke continues to be a beacon of success. The HousingWire Mortgage Rankings show that he ranked No. 7 nationally among the Top Brokerage Originators with $252.6 million in volume across 668 loans. The list focuses exclusively on brokered loan production, isolating performance within the broker channel regardless of other origination channels. Cooke said his team now has 14 people, including eight processors, and most of their business is tied to purchase lending.

“We’re small, but we do a decent amount of volume — probably about $500 million a year in VA business,” he said. “For 90% to 95% of lenders out there, it’s just another box, another program to offer. Who dives into actually training their originators, training their processors on the VA product? Very few.”

Cooke says that World Home Loans currently offers 30-year fixed-rate VA purchase loans at 5.125% with no points, adding that this figure isn’t much higher than recent low points before the conflict in Iran sent rates higher. The company also has five-year adjustable-rate VA mortgages at 4.75% with no points — a product he claims many major lenders don’t offer and many veterans don’t know exists.

And the company expects to build more brand awareness in the near future through a pilot commercial partnership with Military.com.

“They’re probably the most authoritative web domain for the military with the amount of traffic they get,” Cooke said. “We’re working with them to kind of perfect their algorithms for generating leads. They want to build a mortgage and insurance marketplace on their website for vets. They selected us for that, which is a milestone for us as we’re going through the ebbs and flows of the commercial partnership and perfecting performance on both ends.”

Successful career transition

Vipul Hapani was a client at Vema Mortgage when he realized he could help others in his situation — first-generation immigrants aspiring to live the American dream and own a home.

“I was very thankful to my broker for getting me the loan. It struck me: This person is giving happy moments to all his clients. Why can’t I try that?” Hapani said. “The more I helped people, the more referrals I received. In almost six years in the industry, I have not spent a single dollar on marketing. It’s just word of mouth.”

Previously a physical therapist, Hapani brought a personalized approach and multitasking skills to his new career. He scaled rapidly at Vema, securing state licenses and recruiting loan officers before eventually becoming an equity partner.

His rapid growth propelled him to become one of the top brokerage originators in the country in 2025. Hapani ranked No. 3 with $351.5 million in volume across 739 loans, according to HousingWire’s rankings.

Hapani considers purchase loans his bread and butter, noting that refinances ebb and flow with industry cyclicality. That means maintaining close relationships with real estate agents — the partners who “will feed you when the market slows down.”

While he focuses heavily on conventional loans, Hapani has also started originating home equity and non-QM products.

His borrowers are primarily within the Asian community, with an average home price of $600,000 to $700,000 in the mid-tier housing market. Based in Charlotte, Hapani noted that supply issues in North Carolina’s largest market eased significantly in 2025 compared to previous years.

Builders came into the market with a lot of inventory they couldn’t move, so they threw in plenty of incentives for borrowers. “The Charlotte and Raleigh markets are currently oversupplied. There are more sellers on the market compared to buyers right now,” Hapani said.

His service doesn’t end at the closing table. He follows up with clients three weeks after closing to ensure their payment accounts are set up, checks in every six months and conducts annual reviews. For example, he’ll go over their home value, calculate how much equity they have and determine if they need further financial help.

To close loans efficiently, Hapani employs a processing team of nine but relies heavily on lender underwriting teams, who reduce his workload by an estimated 60%. “My main focus is looking at the client’s profile to see if they qualify and what options I can offer them,” Hapani said.

Carving out a niche

Similar to Hapani, top loan officer Thuan Nguyen — the founder and CEO of California-based Loan Factory — leads a production machine powered by roughly 10 loan officers. Each of them are supported by an assistant and a processor, with about 30 people focused on the company’s pipeline alone.

Nguyen told HousingWire that he’s able to spend most of his time on marketing and building systems rather than on direct client contact, relying on his licensed team to handle day-to-day borrower interactions. Automated email campaigns under his name keep his brand in front of past and prospective clients so that when they’re ready for a mortgage, they come back to him.

As an immigrant from Vietnam, Nguyen says that while his clientele is diverse in terms of borrower type, ranging from first-time buyers to real estate investors, about 50% of his clients are Vietnamese.

“I’ve been so strong in the Vietnamese community after so many years — a lot of people know me, so that is my strength,” he said. “Most of my clients are conventional loans, and I need to expand that to FHA, VA and jumbo loans.”

Nguyen has been recognized as a top loan officer for several years running. His motivation comes from what he describes as a “passion” for building better systems and better technology to help people. In HousingWire’s broker rankings, he placed No. 4 with a volume of $304.6 million across 958 loans in 2025.

“The competition is very tough out there, and we need to work harder to grow our business,” he said. “If we stop, if we slow down, our business will slow down. In this market, it is not easy to be successful, and I know that, so that is why I’m not hesitating to build up the right team.”

About Neil Pierson

Neil Pierson serves as Mortgage Editor for HousingWire and is based in the Seattle area. He began reporting on mortgage finance issues in 2017, first as the commercial magazine editor at Scotsman Guide Inc. and then as the company’s editor in chief. Prior to that, he spent 15 years working for community newspapers in the state of Washington.

Flávia Furlan Nunes is HousingWire’s mortgage reporter. Originally from Sāo Paulo, she spent more than ten years working for prominent Brazilian economic outlets before moving to New York City. Flávia has a Master’s Degree in Economics and Business Reporting from Columbia University.

Sarah Wolak is a mortgage reporter at HousingWire. Previously, she was a writer at National Mortgage Professional, where she produced podcasts, anchored news segments, and contributed to several trade publications. Her work has also appeared in Modern Luxury, Voice of America, and The Day Publishing Company.

Let’s bust this longstanding myth right off the bat: “Buy only if you’ll stay 30 years.” Too many of our Veterans and military families have treated that way of thinking like gospel – and lost out on real wealth. The smarter question isn’t whether a home is forever, it’s whether the payment makes sense today. If it does, buying is almost always the right move. Waiting to buy because they’re buying into the this myth means missing years of appreciation, equity growth, and the long-term wealth benefits of homeownership.

Reality: Most Service Members Relocate Every 3-7 Years

Knowing they don’t generally stay in one place forever, many Veterans think buying a home is a mistake. That misconception pushes them into a rental situation; and renting longer than necessary with nothing to show for it when it comes time to move. They’re building someone else’s equity, while at the same time, stand on the homebuying sidelines as prices rise. Vets also miss out on a key wealth-building principle: homes typically appreciate 4–5% per year, even through recessions. And principal paydown and equity growth doesn’t require a decades-long stay.

I embrace the idea that our service members should buy a home rather than rent one. When I work with VA borrowers, I focus on showing them that homeownership – even for a few years – can be a smart financial decision.

Seizing the Opportunity

Delaying a home purchase isn’t just about missing appreciation. It’s about seizing the opportunities that present themselves. Many military markets have strong rental demand, so Veterans can rent out a property or reuse their VA entitlement later. So the trick is structuring the loan correctly to make sure the housing payment fits their life today. That’s where strategy meets flexibility, something too few borrowers are guided on. And something we are uniquely qualified to deliver.

Building VA Loans with Flexibility in Mind

At World Home Loans, every VA loan we structure is designed to help Veterans build wealth no matter when the next PCS comes. That starts with manageable payments and minimizing out-of-pocket cash, so borrowers preserve liquidity. Competitive pricing accelerates equity growth. And choosing locations and property types with strong appreciation and resale potential is key for creating a long-term investment, even if the stay is short.

Many Veterans don’t consider these options until it’s too late. At World Home Loans, the way we look at a VA loan is it shouldn’t be a constraint; it should be a tool for flexibility, growth, and stability. Properly structured, it serves today’s needs while keeping tomorrow’s options open.

Don’t Think Forever Home, Think Forever Wealth

In working in this industry for 20+ years, my definition of what a “good” home investment is for Vets has evolved. It’s no longer about a forever home, it’s about making a financially sound decision that’s right for the buyer. A home doesn’t need to last 30 years to deliver value for Vets. It needs to make sense now, and position the buyer to benefit from appreciation and equity paydown.

For service members who are holding back from buying a home now because they’re worried about moving soon, we say, don’t worry. We tell them to focus on three things: A payment that works today; a property that has strong resale potential; and a loan that preserves flexibility. Homeownership isn’t about permanence—it’s about progress, stability, and making the investment work for Vets. We believe that with the right lending partner and the right VA loan, even a career that demands frequent relocations can be a foundation for wealth. It’s just one of the ways World Home Loans helps Vets achieve Victory on the home front.